http://www.freepressjournal.in/analysis/rn-bhaskar-indian-banks-seek-to-fatten-themselves/1035472

Policy Watch

Indian banks’ disdain for small depositors

Rn bhaskar

Last week was a turbulent one for the banking industry. It began with the country’s largest bank, State Bank of India (SBI), announcing an increase in cash withdrawal charges for its customers. The SBI chairman stated that the charges became inevitable in order to meet the costs of the soaring number of Jan Dhan accounts If that was not bad enough, HDFC Bank’s managing director also announced “I am not a free enterprise, customers must pay me for my services.”

Both statements riled most bank consumers. Their anger was evident in Twitter and Facebook posts. .

Both statements riled most bank consumers. Their anger was evident in Twitter and Facebook posts. .

Bank customers are livid. They believe that both the Reserve Bank of India (RBI) and the government have let them down. Savvy analysts list out nine reasons:

- It may be true that the banks have to bear the additional charges for managing over 40 million Jan Dhan accounts (which are also zero balance accounts). The government compelled Indian public sector banks (PSBs) to take up this job. This will help the government in reducing the leakage of payments made under various subsidy schemes. Logically, therefore, the banks and the RBI should have asked the government to pay this cost. Was this done?

- Almost all non-Jan-Dhan account holders are already under the purview of the income tax authorities. They are already direct tax payers. So why burden them with one more cost? Why is the finance ministry insensitive to the woes of existing tax payers?

- HDFC’s justification is both thoughtless and insensitive. It wants to service its shareholders. The bank evidently forgot that shareholders account for only one-tenth of any bank’s funds. The remaining nine-tenths come from depositors. Is it fair to be more concerned about the one-tenth and not the crucial none-tenth?

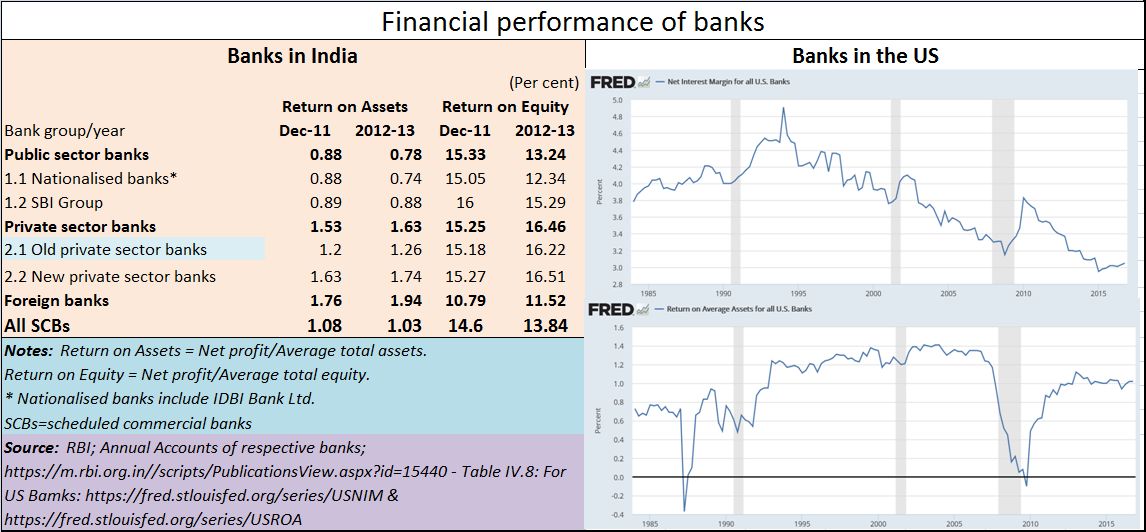

- Consider the chart alongside. Private sector and foreign banks are already making more money than US banks do. The laggards are PSBs. Why should private and foreign banks be allowed to extort more from customers when they are already earning more? Moreover, US banks have are learning to cope with lower returns. Why must Indian private and foreign banks be so greedy?

- There is no denying that PSBs generate lower returns. But that is because of poor business judgement, soaring NPAs and mismanagement. Unfortunately, here too, the government is the biggest culprit. Except for the current government, previous governments have brazenly promoted crony capitalism and loan waivers. They have compelled banks to give loans for projects that everyone knew were unviable enterprises. Sadly, today, only the bankers are being prosecuted, not the legislators who caused this to happen.

- HDFC talks of high costs. The solution should be cost control, right? But look at the fat packages most bankers award themselves. Already, there is a growing unease at the way salaries for the finance sectors have outstripped salaries for CEOs of manufacturing and service companies. This has become a national headache because the best brains are drifting towards the highest paying sectors. Thus, you have IIT graduates moving to the finance sector causing the country a double loss (http://www.asiaconverge.com/2014/10/iits-and-the-seduction-of-finance/). One, the country subsidises their engineering studies. Two, it loses good engineers to a sector that was supposed to be an aid to manufacturing and services. Finance was never intended to be the primary sector in the Indian economy (http://www.asiaconverge.com/2015/12/india-promotes-inequality/).

- The RBI too has failed to rise to the occasion. It refuses to give out comparative bank statistics on senior employee costs and average ATM operating expenses for public scrutiny. Moreover, as is evident from the charts, it has failed even to provide the latest financial figures. One can get 2015 data for US banks, but only FY2013 data for Indian banks. The finance ministry has done worse. It has even failed to provide the latest statistics as part of its economic survey (http://www.asiaconverge.com/2017/03/the-missing-data-tables-in-economic-survey-2017/).

- It is evident that the finance sector will be the biggest beneficiary of digitisation. Estimates show that epayment commissions could be as high as 20% of India’s GDP (http://www.asiaconverge.com/2017/02/epayments-spell-boom-times-for-financial-intermediaries/). Then why hasn’t the RBI tightened its norms for the epayments sector (http://www.asiaconverge.com/2017/02/epayments-the-rbi-the-cabinet-secretary-and-the-govt/)?

- Finally, why have the government and the RBI been silent about unfair practices promoted by government entities themselves (http://www.asiaconverge.com/2017/02/epayments-the-rbi-the-cabinet-secretary-and-the-govt/). Consider, for instance, how municipal corporations still issue receipts for sums which do not include the transactions fees that customers must pay? Indian rules require vendors to include all costs on their receipts. Why have government agencies been the biggest defaulters on this front?

The proposed surge in bank charges is therefore odious. Unfortunately neither the government nor the RBI has shown the sagacity to ensure that hapless customers are not penalised.

{kind=link}

COMMENTS