ePayments and the scam potential

Try paying a bill of the MCGM (Municipal Corporation of Greater Mumbai) — the epayments way — through its web portal. It will be a vexing experience.

Half the payment gateways do not work This could be deliberate – one is not sure. But it could be a clever way to mask the channeling of all epayments through the preferred gateway. The fact that the exercise fails just after you give your OTP [one-time-password] code could be a good way to ensure that nobody really finds out that the gateway does not work till he is the actual consumer.

Half the payment gateways do not work This could be deliberate – one is not sure. But it could be a clever way to mask the channeling of all epayments through the preferred gateway. The fact that the exercise fails just after you give your OTP [one-time-password] code could be a good way to ensure that nobody really finds out that the gateway does not work till he is the actual consumer.

The only credit card company that is promoted on the MCGM website is American Express. There is no mention of RuPay, Mastercard or VISA or any of the nationalized banks. A few private sector banks are listed. Yet the transaction usually does not succeed.

And when the attempt to epay does succeed, you find that you have ended up paying a commission to PayU.in, This is a private player whose ownership details are not given on its website, though details of its management team can be found (https://corporate.payu.com/leadership-team). The commissions can be as high as Rs.5.75 for a Rs.111 transaction. So on a Rs.100 bill you end up paying 5.2%.

The amounts debited to the consumer do not appear on the MCGM receipt. So there is no way for the MCGM admin to know which gateway has been preferred. But your bank debit reflects the higher sum and the party receiving the commission. And considering there are at least 5 million families, at least a million businesses who may have to pay all their Shops & Establishment charges, Octroi fees, Sales Tax, Property cess and water charges through the portal the private booty accruing to payU.in can be substantial.

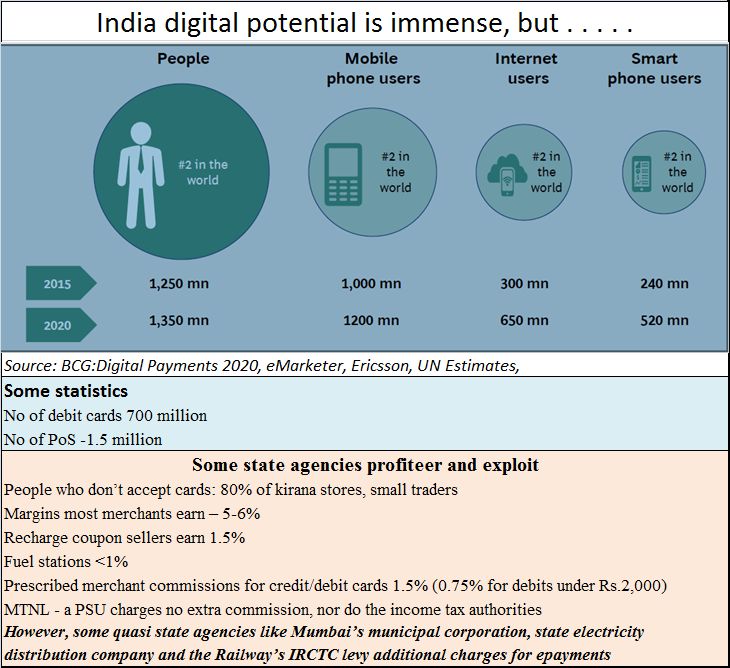

Then take the Maha-Vitaran, the state government owned power distribution company (discom). It too has an epayment gateway with select payment partners. And its bills too come with a 0.9% “convenience” surcharge. And it routes many of its transactions through Bill Junction, Bill Desk and Tpsl-india. Like MCGM, the amount paid to service providers does not get reflected in the actual receipt the customer gets.

Ditto with IRCTC, which also levies a huge Convenience Charge of Rs.46 per transaction (up from Rs.22 it charged earlier) plus the commission the payment gateway charges. The rates of Axis Bank are the lowest (1.65% compared to the highest charge of 1.9%). But transaction charges are not included in the receipt. IRTCTC is a monopoly (only it is authorized to sell tickets for Indian Railways). Hence it can earn around Rs.2.52 crore daily as service charge from the average sale of 5.48 lakh tickets every day (during FY16 it sold 200 million tickets (http://www.ibtimes.co.in/irctc-aims-earn-20-more-online-ticket-sales-fy17-677800).

In all the three cases above, the agencies enjoy a near monopoly. There is no competition, because none is allowed – at least till now. And these are just three instances. There could be countless more.

In all three cases the convenience charge collected from consumers is actually convenience for the private party and for the quasi-government monopolies. Ideally, they should be emulating government-owned MTNL or like private sector Tata Power. They don’t add service charges or transaction charges to customers. On the contrary they even offer small rebates if the money is paid in time. In fact, epayments provide more convenience to the enterprises than to consumers, as the need to reconcile amounts with tickets sold is eliminated. Convenience or service charges are therefore nothing but repugnant!

In most countries such additional charges would have been labeled as a misuse of powers that a monopoly has usurped for itself. Unfortunately, that has not happened in India.

And that is why the government needs to appreciate the perils in implementing epayments across the country.

- It must begin with government and quasi government organizations. This must be done without surcharges, convenience charges or transaction charges billed to customers. All of them must offer service providers like RuPay, VISA and Mastercard, and also list debits to the accounts of all nationalized banks. All charges must be mentioned on the receipt.

- There must be an epayment regulator to whom anyone can complain in case of a perceived violation of norms.

- Adjudication of grievances must take place within a week of the dispute being filed. This is because while normal financial transactions leave a paper trail, epayments have a digital trail that can vaporize unless frozen promptly under secure conditions. And it is unfair to expect a small income earner to watch his money misappropriated, and then be told that he will have to wait 10 years for a verdict, and also be told that he will need a lawyer and pay court fees. Without this facility, the imposition of epayment on all people can be highly perverse.

- The regulator should also be equipped to understand a bit about the technologies involved, so that he is in a position to comprehend the nature of technology-related fraud. It shall be the responsibility of this regulator to ensure system audits, and to hold educational sessions for the police and the judiciary as well.

- Suitable amendments to the Indian Penal Code must be introduced to make the penalties for fraud and misappropriation very stiff. So long as the cost of non-compliance is lower than the cost of compliance, there will always be an incentive to defraud people.

If the government cannot ensure all this, pushing epayments is both dangerous and citizen unfriendly.

{kind=link}

COMMENTS