https://www.freepressjournal.in/analysis/debt-under-control-good-now-for-economic-growth/1387659

Debt and economic growth

Talk of debt is in the air. Everybody is talking about it. In fact there is a CARE Ratings study which looks at state and central government debt (Debt Profile of Centre and State Governments – of 8 October 2018). It is quite insightful.

While there is a great deal of gloom on the economic growth front, the Indian government appears to have managed its debt exposure fairly well – both at the centre and at the state levels.

While there is a great deal of gloom on the economic growth front, the Indian government appears to have managed its debt exposure fairly well – both at the centre and at the state levels.

Bright side

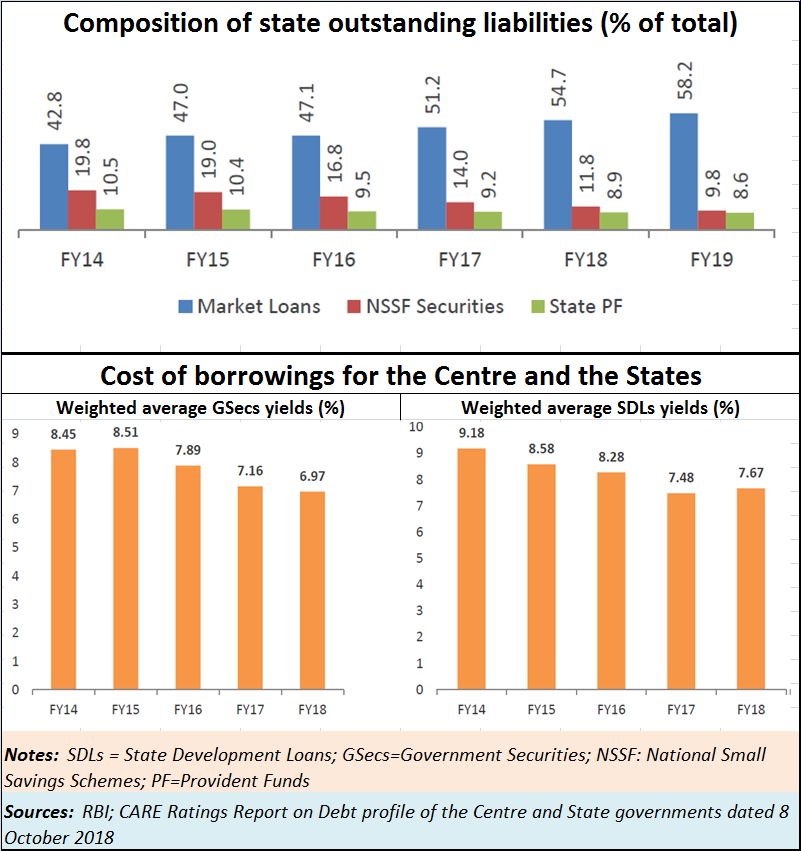

The CARE report points out how the central government has managed to contain its debt burden, and even hopes to reduce it. Moreover, it has also managed to reduce its cost of borrowings (see table). On the other hand, state governments saw their debt burden increase as well as their cost of borrowings.

The report states that the Central government has managed to keep its borrowings broadly stable within the range of Rs. 3.3 lakh crore to Rs. 3.6 lakh crore during the last 5 years. For the period, 1 April- 28 Septtember 2018, the gross market borrowing for the central government was Rs. 2.8 lakh crore, 22.7% lower than the comparable period previous year.

For state governments, however, the gross market borrowings till date have witnessed a sustained increase during FY14 to FY18 from Rs. 75,938 crore to Rs. 1,77,939 crore at a CAGR of 23.7%, following which it has moderated during the current year (FY19) to Rs. 1,57,502 crore.

Another interesting difference between the borrowing patterns of the Centre and states is that the central government has tended to frontload its borrowing during the first half of the year. In contrast, states which are usually unprepared for their budgetary requirements and needs tend to borrow a larger proportion of their targeted amount during the second half of the year.

Additionally, the Central government has both internal (95%) and external (5%) outstanding liabilities unlike state governments which only have internal outstanding liabilities. The total outstanding liabilities of the Centre government at Rs. 91.9 lakh crore in FY19 is double that of the state government liabilities of Rs. 45.4 lakh crs. The outstanding liabilities of the state governments have witnessed a much faster CAGR of 12.9% than the CAGR of 9.7% of the Centre.

The dark side

That was the good part of the news. But there is another side to the debt story as well.

The first is that the centre has not provided for several areas that should have been provided for. Notable among them is the non-performing assets of the banks and the desperate need to recapitalize the banks. Second is the unwillingness to let bad banks like IDBI find a private sector white knight. Transferring it to the Life Insurance Corporation (LIC) could be a decision that could backfire badly (http://www.asiaconverge.com/2018/09/bank-mergers-abracadabra-mess-vanishes/).

Ditto when it comes to potential failures like IL&FS. The government hasn’t yet come out with a cogent explanation on why IL&FS needs to be bailed out by LIC and not by private investors through the NCLT route. Nor is the government willing to explain why there has been no move to have a forensic examination first. Is it because the government does not want the audit to reveal dark secrets of the nexus between powerful people and IL&FS projects? That report needs to be made public, since public funds are being used to salvage this organisation which is neither-fish-nor-fowl. IL&FS tried to play the role of a financial institution without the tag of one. It acted like an NBFC (non banking financial company) but was not regulated (in its entirety) either by the RBI or SEBI.

Provisions should have been made for such bailouts. That hasn’t been done till now

Then there are schemes announced by the government for which too inadequate allocations have been made. A good example is Ayushman Bharat – the world’s largest health insurance programme – meant to cover 10.74 crore families (https://www.india.gov.in/spotlight/ayushman-bharat-national-health-protection-mission) . But the provision is just Rs.1,200 crore (http://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=1518544).

That translates into a little more than Rs.100 per family annually If the states are to bring in the rest of the money, state indebtedness will increase. If neither side provides the funds, the scheme will exist only on paper.

And finally, there is the issue of economic growth. The government complains about increasing oil import bills. But hasn’t this author been crying hoarse for the past four years about the need to tap waste-to-methane (http://www.asiaconverge.com/2018/04/shit-can-mean-big-money/) and rooftop solar in a more aggressive way. Had that been done, it would have created at least 80 million jobs and saved the country its soaring import bills (http://www.freepressjournal.in/analysis/the-actual-employment-potential-r-n-bhaskar/1350110).

Clearly, the debt story does not absolve the government of everything.

{kind=link}

COMMENTS