India’s textile industry: where does it go from here?

Rn bhaskar

The textile industry is the backbone of India’s foray into the industry era. It was this sector which actually defined India for a couple of centuries. And it still remains one of the largest employers in the country.

Much of the industry is synergistic with apparel (the obvious value-added sector after the yarn is woven into fabric). It is labour intensive. But, its growth has been stunted, especially in areas related to exports. Yet, the odds still favour India.

Much of the industry is synergistic with apparel (the obvious value-added sector after the yarn is woven into fabric). It is labour intensive. But, its growth has been stunted, especially in areas related to exports. Yet, the odds still favour India.

India’s apparel market is large – worth $57 billion. But that is just 39% of China’s exports.

One problem could be this industry’s excessive reliance on government support. It has also been over-dependent on the US and European markets. But, most critically, it has been hobbled by the government’s labour policies, and its on-again-off-again rules favouring man-made fibres or cotton or blended fabrics at various times. The absence of a cogent long-term policy that could help the country has prevented the industry from capitalising on its native strengths.

Restrictive labour policies compelled the industry to opt for automation at a time when capital was at least twice as expensive as elsewhere in the world (import duties and implementation delays pushed costs up). As a result, the industry could not benefit tremendously from either automation or cheap labour.

It is only now that the government is waking up to the need for a flexible labour policy for textiles (and for several other industries). It has allocated funds for the industry’s modernization and is working on policies that allow for a flexible workforce.

The need is urgent. In fact, even the World Bank highlights the opportunities that lie ahead. In its report of March 2016 (see links http://fisme.org.in/document/Stiches-to-Riches.pdf and http://elibrary.worldbank.org/doi/book/10.1596/978-1-4648-0813-5), it points out

- South Asia must create good-quality jobs for a rapidly expanding young population and bring more women into the labor force.

- The apparel sector in South Asia is labor intensive, employs more women on average than other manufacturing sectors, and provides jobs that allow for the acquisition of skills.

- Apparel already constitutes approximately 40 % of manufacturing employment. And, given that much of apparel production continues to be labor intensive, the potential to create more and better jobs is immense.

- Despite these development benefits, the sector has not reached its full potential because of inefficiencies that affect its competitiveness.

- As a creator of jobs that are “good for development” and an illustration of the distortions that stifle productivity in light manufacturing in South Asia, this sector merits careful analysis.

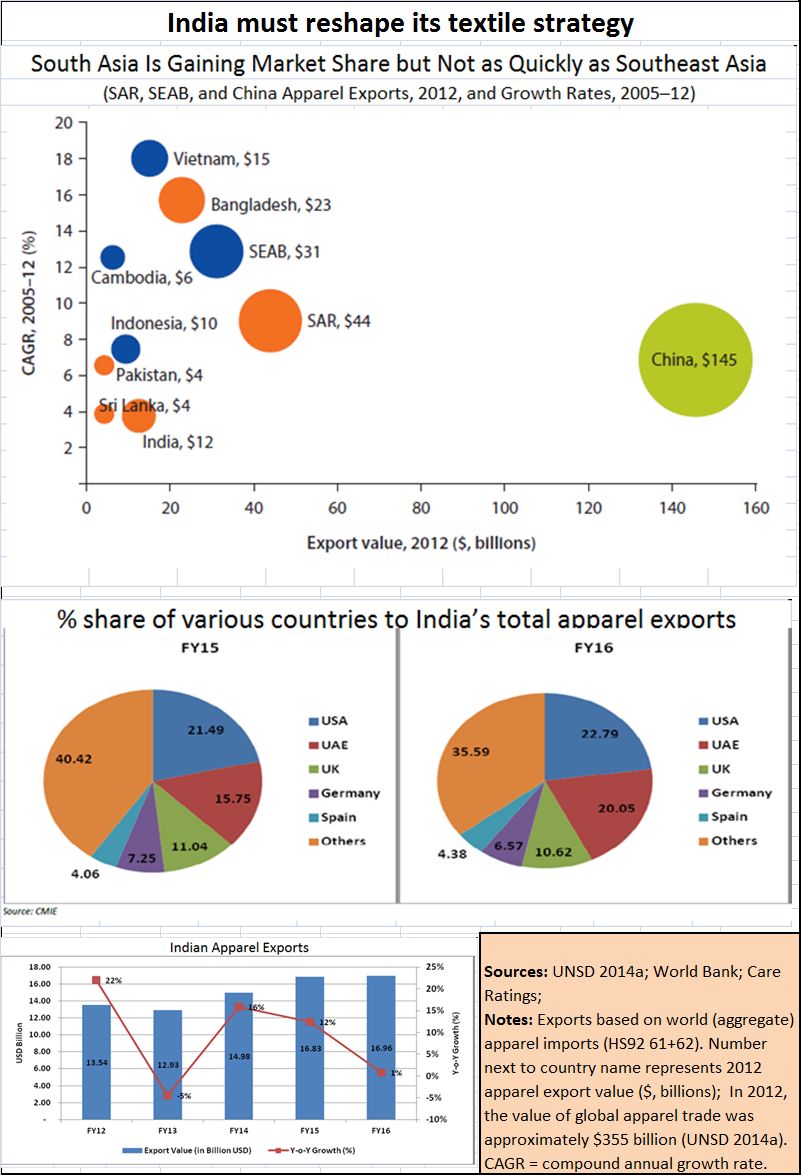

The biggest opportunity for India and other Asian countries is the inevitable drifting of the apparel trade away from China. But with labour costs increasing, this $145 billion market will seek out other production centres. Many Asian players could grab a bit of this pie.

As the World Bank report puts it, “The potential decrease in Chinese exports presents a huge opportunity for South Asian countries—which currently account for 12 percent of global apparel exports—prompting a lot of debate about how best to position the region and generate good jobs . . . . Indeed, our estimates suggest that a 10 % increase in China’s prices would boost South Asian exports between 13 and 25 %, although the gain would be even bigger for Southeast Asia (between 37 and 51 %).”

A recent report by CARE Ratings (October 18, 2018) on this industry makes reference to data published by Ministry of Textiles (in its annual report 2015-16). India is ranked as 6th largest exporter of apparel in the world after China, Bangladesh, Vietnam, Germany and Italy. But the CARE report also points out how India’s biggest benefit could be its domestic market which is worth more than $40 billion.

Compare this with the domestic market of just $3 billion for both Bangladesh and Vietnam combined. If production for the domestic and export markets are considered, India’s value jumps to $57 billion, compared with $24 and $20 billion in Bangladesh and Vietnam, respectively. Moreover, growth in the organized retail industry is expected to pick up in the next two years with increasing GDP per capita.

Clearly, the trick would be to get the industry improve the quality and price of its offerings to the domestic market and thus increase its export edge. But with the industry complacent, and with its offerings to the domestic market too poor in quality and too steep in price, this edge has not been exploited. This must change. There is nothing like a vibrant domestic market to galvanise exports.

One hopes that the government’s policies prod the industry towards expanding the domestic market. That would benefit consumers within the country, and sharpen India’s apparel export thrust as well.

{kind=link}

COMMENTS